Northeast and California counties top list of ‘most vulnerable’ markets

A new ATTOM report looked at affordability, foreclosures and other factors to determine the most and least vulnerable housing markets among nearly 600 counties.

Key points:

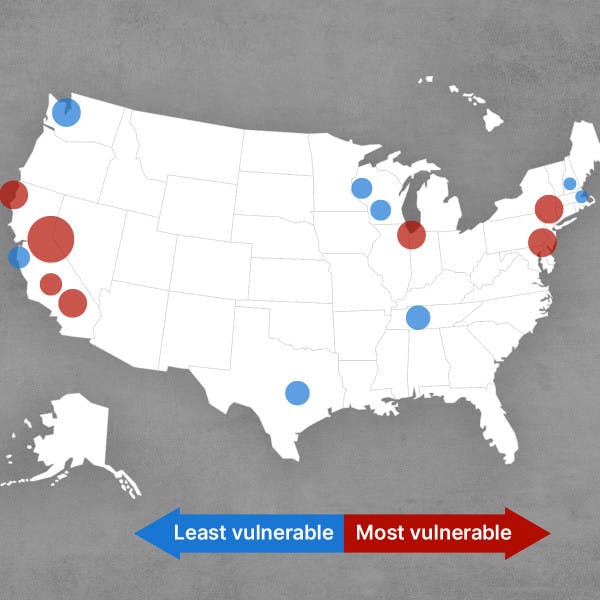

- The most vulnerable markets were centered around major metros including New York, Philadelphia and Chicago, as well as several counties throughout California.

- Regions considered less vulnerable to the impacts of a slowing economy include the South, with Tennessee leading the way.

- Even the markets listed as vulnerable aren’t expected to have big drops in home values under current economic conditions.

As the housing market continues to slow nationally, several areas of the U.S. are especially vulnerable to economic declines.

New Jersey, Illinois, Delaware and central California have the highest concentration of at-risk housing markets in the country, according to a new report from ATTOM. The report looked at a variety of factors in the third quarter to determine vulnerable areas, including home affordability, underwater mortgages, foreclosure rates and unemployment levels.

Markets considered the least vulnerable during the third quarter were mainly in the South, Midwest and Western areas outside California.

Vulnerable markets not likely to experience a housing crash

The report pointed out that despite the vulnerability gap across markets, "an imminent, major fall in home values or equity" is unlikely.

Among the 50 most at-risk areas, eight are in and around New York City, seven are in the Chicago metro area, four are around Philadelphia, and nine are spread across northern, central and southern California.

These areas share a number of traits, including poor affordability and relatively higher foreclosure rates, said Rick Sharga, executive vice president of market intelligence at ATTOM. Mortgage payments consumed more than one-third of average local wages in 33 of the 50 vulnerable counties, according to the report.

Sharga doesn't expect any of the areas classified as "more vulnerable" to experience surging foreclosures or plummeting home values if the housing market slowdown remains in place in the near term. However, those markets will probably take more time to recover once the slowdown is over.

Unemployment and low affordability key factors in vulnerable areas

Of the measures used in the analysis, Sharga said unemployment and unaffordability are probably the two most likely to trigger problems.

"Unemployment tends to reduce the number of home sales, and also leads to increased numbers of foreclosures," Sharga said in an email. "Unaffordability — as we're seeing since mortgage rates doubled this year — can bring home sales to their knees, and ultimately could lead to prices dropping significantly in a market correction."

Though the number of underwater mortgages nationwide remains small relative to the 2008 financial crisis, at least 7% of home mortgages were underwater in the third quarter in 28 of the 50 most at-risk counties. Peoria County in central Illinois topped the list with 16.8% of mortgages underwater, followed by Tangipahoa Parish, Louisiana (about an hour north of New Orleans) at 15.7%. Saint Clair County, Illinois (near St. Louis) was third on the list with 15.1% of mortgages underwater.

For context, around 30% of homeowner mortgages were underwater in 2008 across the U.S., compared to 5.7% today.

Southern counties dominate the list of less-vulnerable markets

Among the markets less at-risk for housing market declines, Tennessee led the way with six counties. The report found that 21 of the 52 least-vulnerable counties were in the South, while 15 were in the Midwest. Minnesota, Wisconsin and New Hampshire all had several counties on the list. Among major metros, Seattle, San Jose, Boston and Austin were considered to be at lower risk.

Most of the less vulnerable counties had more affordable homes in relation to prices and wages in the area. Generally speaking, an affordable mortgage payment is one that requires less than one-third of the average local wages. Markets with affordable payments include Morgan County, Alabama, where mortgages require 20.4% of household income; neighboring Limestone County, Alabama (25.5%); and Saint Louis County near Duluth, Minnesota (22.3%).